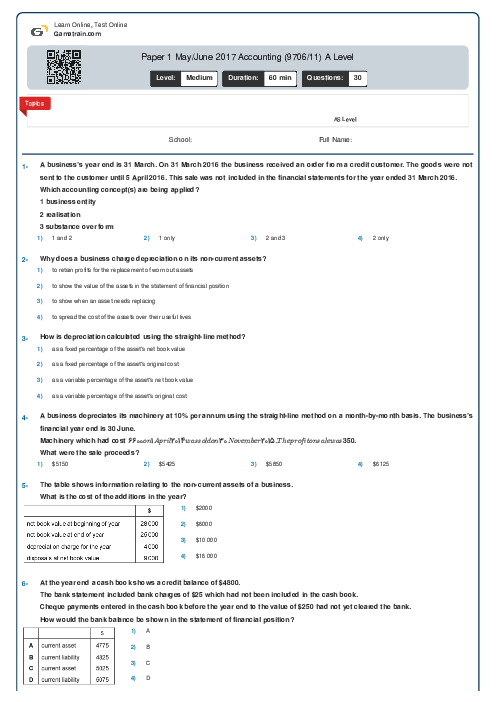

Paper 1 May/June 2017 Accounting (9706/11) A Level

Cambridge

AS & A Level

Accounting (9706)

شهریور

2017

شامل مباحث:

AS Level

تعداد سوالات: 30

سطح دشواری:

متوسط

شروع:

آزاد

پایان:

آزاد

مدت پاسخگویی:

60 دقیقه

پیش نمایش صفحه اول فایل

Arefe Naderlouei

Arefe Naderlouei

ثبت شده در

5 بهمن 1401

Which statements concerning the use of a budgetary control system are correct?

1 Managers should receive a copy of the budget.

2 Managers should agree with the aims and objectives of the budget.

3 Managers should be consulted when the budget is prepared.

4 Managers should be committed to attaining budget outcomes.

پرسش و پاسخ های مشابه

سوال کنید یا به سوالات دیگران پاسخ دهید ...