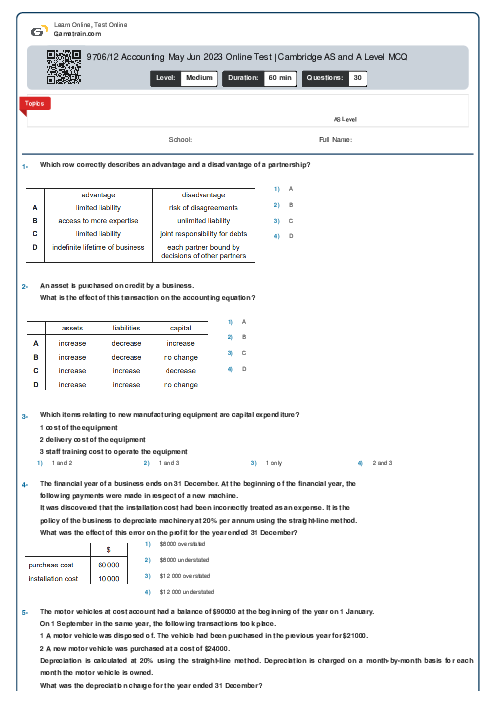

9706/12 Accounting May Jun 2023 Online Test | Cambridge AS and A Level MCQ

Cambridge

AS & A Level

Accounting (9706)

شهریور

2023

مشاهده نمونه سوال

شامل مباحث:

AS Level

تعداد سوالات: 30

سطح دشواری:

متوسط

شروع:

آزاد

پایان:

آزاد

مدت پاسخگویی:

60 دقیقه

پیش نمایش صفحه اول فایل

Neda Bani

Neda Bani Iga is worried that her book-keeper may have been forgetting to record credit notes received.

What should she do to find out?

1- check purchases ledger balances against statements of account

2- extract a trial balance showing individual purchases ledger accounts

3- prepare a purchases ledger control account

پرسش و پاسخ های مشابه

سوال کنید یا به سوالات دیگران پاسخ دهید ...