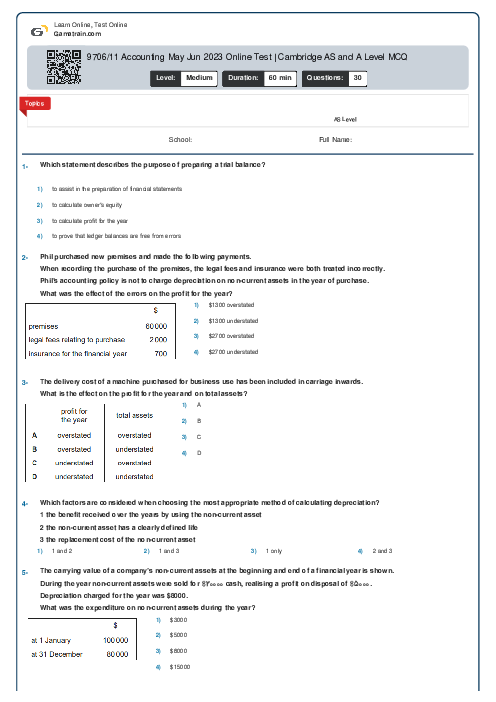

9706/11 Accounting May Jun 2023 Online Test | Cambridge AS and A Level MCQ

Cambridge

AS & A Level

Accounting (9706)

شهریور

2023

مشاهده نمونه سوال

شامل مباحث:

AS Level

تعداد سوالات: 30

سطح دشواری:

متوسط

شروع:

آزاد

پایان:

آزاد

مدت پاسخگویی:

60 دقیقه

پیش نمایش صفحه اول فایل

Neda Bani

Neda Bani A business makes a provision for doubtful debts of 4%. At 31 March 2021 the value of trade receivables after deducting the provision was $\$ 153600$. For the year ended 31 March 2022, there

was an increase of $\$ 960$ in the provision for doubtful debts.

What was the value of trade receivables at 31 March 2022 after deducting the provision for doubtful debts?

پرسش و پاسخ های مشابه

سوال کنید یا به سوالات دیگران پاسخ دهید ...